John Twohig/iStock via Getty Images

SBA Communications Corporation (NASDAQ:SBAC) is a leading owner and operator of wireless communication infrastructure. There was some news at the end of August from AT&T (T) that sent SBAC’s stock price down. You can read that news here on the AT&T website. I’ll be breaking down the main points of this story so investors can have a better picture of what’s going on.

In short, this wasn’t a big negative for SBAC. Now let’s get into the long answer.

Why is the FCC involved?

Why was there an inquiry from the FCC? I believe it was because EchoStar (SATS) was failing to deploy the bandwidth effectively. Companies bidding on the “rights” for bandwidth do not have the “right” to squat on that bandwidth. It must be deployed to benefit the citizens. Since SATS was not deploying it effectively enough (allegedly), they sold it to AT&T.

This came up on the investor call as well. AT&T apparently paid about $7 billion more to purchase the spectrum than EchoStar paid when they purchased it.

Price to AT&T: $23 billion.

Profit to EchoStar: $7 billion.

EchoStar’s original cost: Implied $16 billion.

EchoStar Share Price

The following math uses an approximation of 287.8 million shares outstanding.

Before the deal, EchoStar was trading around $29.62. Market cap of common equity = $8.5 billion.

Today, EchoStar is trading around $56.15. Market cap of common equity = $16.2 billion.

Increase in EchoStar’s total enterprise value (equity + debt) = About $7.7 billion.

Given that EchoStar’s value is up by about $7.7 billion following a profit of $7 billion on the spectrum (should be pretax), we can reasonably assume that EchoStar investors were valuing the spectrum somewhere around $16 billion.

The Press Release Plans

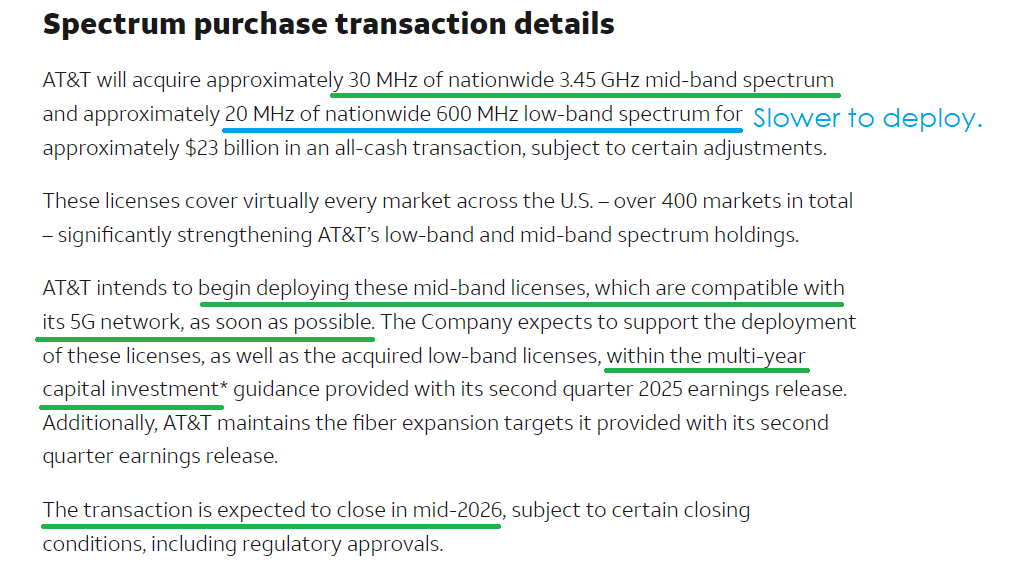

In the press release, AT&T emphasized that they would be deploying the 3.45 GHz spectrum as quickly as possible. There will be a modest delay in getting the 600 MHz spectrum active.

AT&T

That makes sense because the 3.45 GHz fits very well with what AT&T is already using. The 600 MHz spectrum will require some adjustments to equipment. Management says some of their equipment was nearing end of life anyway, so upgrading the equipment to also cover that spectrum should be pretty efficient.

A Quick Note: I’ll just pause here to note that prior commentary from tower REIT executives indicates that installing new equipment to cover more spectrum requires amendments which increase rent.

It sounds like it will take a couple of years as AT&T deploys that 600 MHz spectrum. It’s quite a bit of spectrum requiring hardware adjustments, so it’s no surprise that it would take time to do all of those upgrades.

The Revenue Case for AT&T

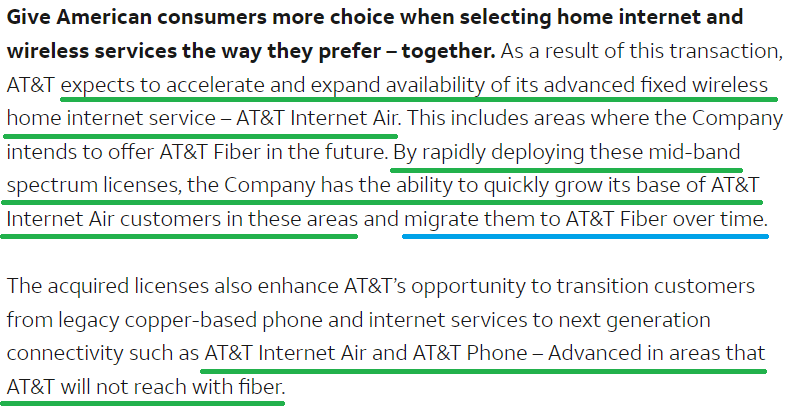

AT&T highlights this as a way to expand availability of fixed wireless home internet service:

AT&T

That’s not bad for the towers either. When AT&T Internet Air gains new customers it puts more traffic on the airwaves. That’s better than having that traffic running over cable. Eventually AT&T would like to move some of those customers over to fiber, but AT&T even acknowledges that many customers will never be reached with fiber.

This emphasis on AT&T Internet Air should be positive for the cell tower REITs because it represents AT&T looking to take market share away from the typical internet service providers. It results in more demand for cell towers by shifting more home internet connections to run on cell towers.

Why Would Analysts Care About EchoStar?

In theory, EchoStar might reduce the amount of tower assets they lease if they are going to run more of their service through AT&T’s network. The agreement to utilize AT&T’s network was part of the deal that resulted in AT&T agreeing to pay $23 billion. It may not have been a large part, but it was a consideration (per management’s commentary):

Yes, the short answer is that we ultimately expect there’ll be incremental value that’s generated from the Boost relationship moving forward, and that’s part of the contribution as to why we think this has been a good move for us. It’s a full package and we view this as a full package, and they all work together.

The Core Factor

The downgrade for SBAC really doesn’t appear to be driven by this particular event.

There’s a challenge from international churn, but that’s been a known factor for quite a while.

SBAC doesn’t have data centers (like (AMT)) and doesn’t have a structural transformation (like (CCI) eliminating fiber). But those aren’t new surprises.

Allow me to paraphrase the remaining argument against SBAC:

SBAC’s price rallied year-to-date because of improved expectations for domestic leasing. Those expectations were based on management raising guidance and talking about an increase in carrier application volumes.

The bears appear to be doubting management’s guidance. I am not.

What Did SBAC’s Management Say?

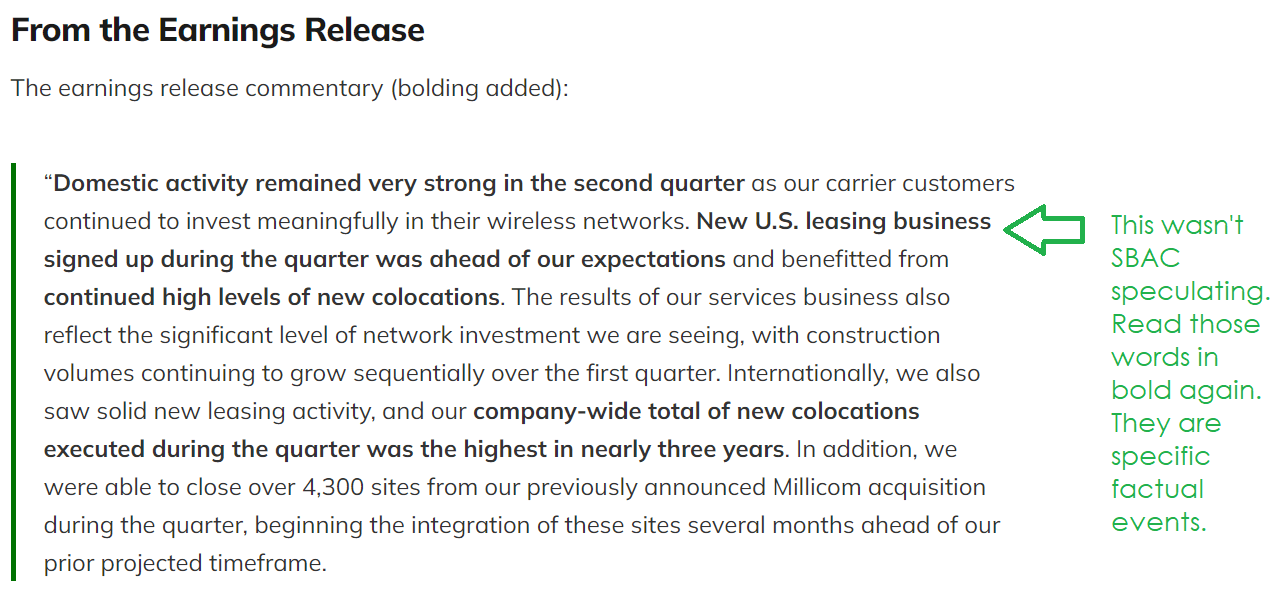

I pulled up our Q2 2025 SBAC Update because I knew it would have the most pertinent info. Here’s the quote:

SBAC

Well, it sure looks like SBAC was talking about leases that were signed. Those are contracts. It isn’t just carriers inquiring about potential leases. It’s signed contracts.

But What if AT&T Reduces New Contracts?

SBAC has an arrangement with AT&T to establish minimum volumes for leases. But SBAC would always like to sign leases for more than the minimum amount of locations.

What if this deal causes AT&T to sign fewer leases over the next several years?

Is that theoretically possible? Sure. But it’s the opposite of management’s commentary about deploying the mid-band spectrum “as soon as possible” and deploying the low-band spectrum “within the multi-year capital investment guidance provided with its second quarter 2025 earnings release.”

I wasn’t able to find a single comment from AT&T suggesting they were cutting back on plans to deploy spectrum. Instead, I found this quote:

The acquired licenses will allow AT&T to continue to be a leader in wireless through enhanced 5G coverage, even greater reliability and faster speeds.

Were they going to achieve greater reliability and faster speeds by buying spectrum and not deploying it?

On the call with investors, AT&T’s CFO said:

Specifically, we expect it will drive incremental service revenue and EBITDA within the first 24 months following deal close, with accretion to adjusted EPS and free cash flow expected in year 3, when the anticipated growth in EBITDA will more than offset the incremental interest expense and capital investments that we will incur as a result of the transaction.

That was part of his prepared remarks. He is very specifically talking about growing service revenue and EBITDA to more than offset the interest expense. Were they going to grow service revenue and EBITDA by squatting on the spectrum?

Conclusion

I don’t see a big negative for SBAC here. AT&T didn’t sign a huge leasing agreement for satellites. They purchased a huge amount of spectrum. They want to use that spectrum to expand their AT&T Internet Air segment. That doesn’t reduce their need for towers. It transitions even more of the market for “home Internet” to going through cell towers. I maintain a Strong Buy outlook on SBAC.