It’s time to highlight the iShares 0-3 Month Treasury Bond ETF (NYSEARCA:SGOV).

I’ll sum it up briefly:

- Simple ETF. It doesn’t get much easier than this.

- The investments are short-term Treasuries.

- Duration is minimal.

- Credit quality is exceptional because it’s Treasuries.

- Volatility is about as close to none as we can get while still having ex-dividend dates. Nearly the entire move in the share price is just accruing dividends and paying them out.

- Since ETFs focused on Treasury bills are not particularly unique, the expense ratio is very important. The expense ratio is 0.09%, which is very good for this type of ETF. While I always want to see expense ratios go lower, this is one of the best for what it does.

- If you know of any that do the same thing as SGOV but with an expense ratio under 0.05%, let me hear about it in the comments.

You’re still here reading? Alright, I’ll try to put some more words in this article. Maybe even an image or two.

The Dividend

One of the main reasons for using SGOV is that you want the dividends. You’re dealing with Treasuries. Treasuries are better for taxes than dealing with corporate bonds. At least for most Americans.

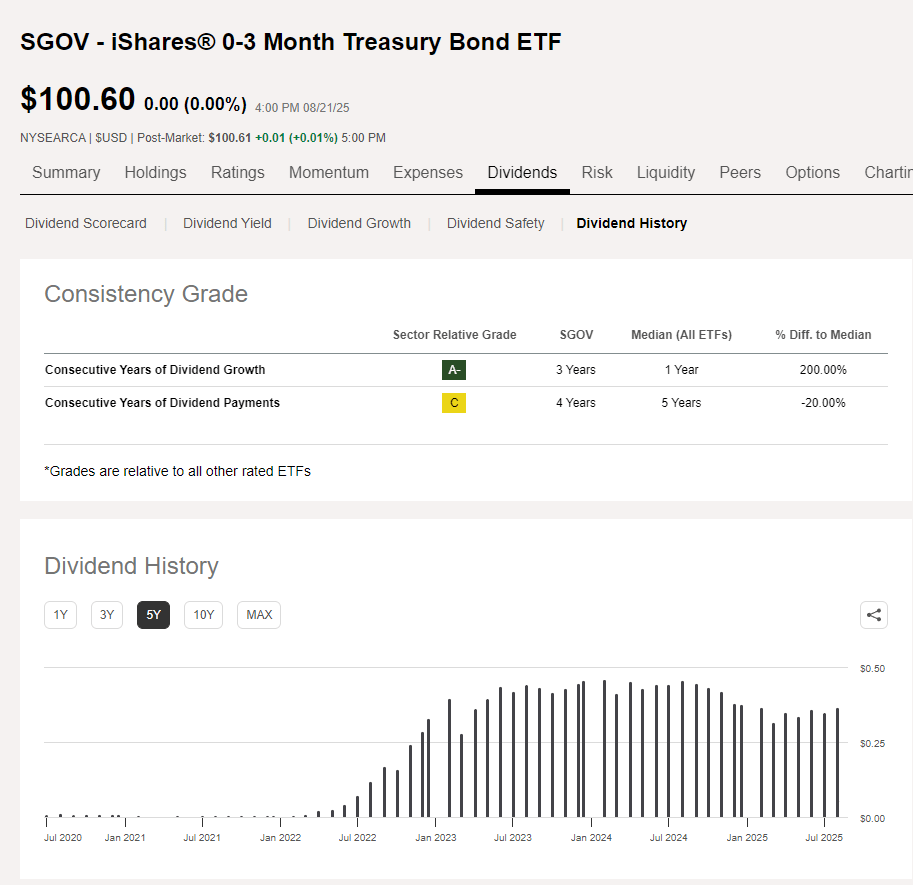

So let’s take a look at the dividends:

Seeking Alpha

Not bad. You can see right away that the dividend started to dip. That’s because the short-term rates were reduced.

Lower short-term rates mean a lower rate when it buys new Treasury bills.

Price Stability

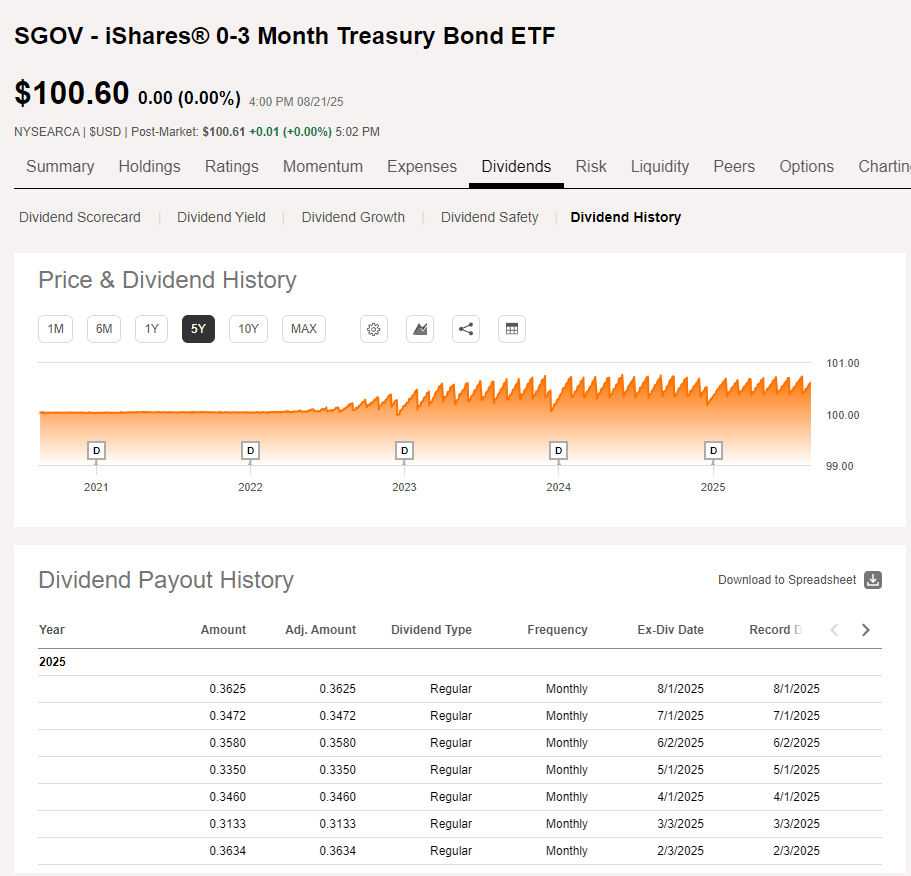

I think this next chart really helps to explain it:

Seeking Alpha

Ignore that the chart only shows the dividend once per year on the price section. It’s actually paid out monthly, as you can see in the table part of the image. Those dividends are the reason that the price goes up and down.

It skips a January payout, and it pays out twice in December. That’s why the pattern looks a little funky.

Why was it so smooth before 2022? Because short-term rates were basically nothing. When the dividend is basically nothing, there’s no reason for it to move up and down with the dividend accrual and ex-dividend date.

I use three ETFs for my cash:

Are these the perfect choices? Perhaps not. But it’s close enough to work pretty well. I’m sure there can be a great discussion in the comments about which ones are the very best.

Many investors may not realize how much they are throwing away by holding their cash in a checking account. Maybe you went around hunting for the bank that would offer you a better rate on your cash. That’s fine if you did.

It’s not something I want to spend my time on. Instead, I keep minimal cash in my checking account and a bunch of cash in short-term Treasury ETFs.

Given that I can usually keep my checking account balance below $10k (other than just before I send in my prepayments for taxes), it isn’t worth fussing about which bank will give me a better rate on checking. I can just keep my excess in Treasury bill ETFs.

OK, what I’m saying is I’ve been too busy to stop using USAA. They were outstanding about 20 years ago. Maybe even 15 years ago. Now just a dim shadow of their former glory.

How Do You Use SGOV?

First and foremost, stop thinking that this is an investment. It’s not an investment. SGOV is a cash alternative. It’s extremely liquid. The price is extremely stable. It pays an attractive yield.

Yes, you can hold SGOV in your portfolio. I do. But I just label it as “cash.” I label all of my Treasury Bill ETFs as “cash.” For me, there isn’t much difference.

If you have a huge surprise bill, what do you do?

You put it on your credit card!

No, that wasn’t being sarcastic. You put it on your credit card to get your cash back rewards (or miles if that’s how you roll) and then you pay that card off in full before you incur a dime of interest. If you’re paying interest on credit cards, I don’t even know what you’re doing reading about these ETFs.

If you’re paying credit card interest, you don’t need my article. You need Dave Ramsey yelling to eat cat food until you have savings or something like that. That’s his thing, right? Cat food? No? Look, I don’t listen to his show. If he yelled about eating cat food, then I probably would watch it.

New idea for a YouTube channel? You make YouTube videos where you take calls and yell about eating cat food. I will absolutely give your channel a shot.

Life Lesson: Don’t pay 30% in non-deductible credit-card interest just to earn 4% in taxable interest.

3 Types of Idle Cash

I have three types of idle cash.

- Idle cash that I may need for personal expenses.

- Idle cash in my business account because I’m not insane.

- Idle cash in my portfolio between investments.

Which kind should I invest in short-term Treasury bill ETFs?

All three of them.

If I might need the cash in under a month, then it can sit in checking and earn peasant interest rates. Otherwise, I’ll take the Treasury Bill ETFs.

Seriously, if you’re sitting on $30k in checking (not even enough to be a proper safety fund), you’re missing out on over $1k in interest per year. At least if your checking account interest rates are as low as the ones I’m getting from USAA.